Disability Insurance

Protect your paycheque

Disability insurance works when you can’t. It can give you tax-free monthly income to help pay expenses if an illness or accident stops you from working.

Monthly income

Payments replace part or all of your paycheque each month.

Guaranteed

Your premiums are at guaranteed rates for your coverage until age 65.

Personalized

Customize your personal disability plan to suit your personal needs.

What is Disability insurance?

It can give you a tax-free monthly payment to help replace your income and cover your expenses if an illness or injury keeps you from working. While a disability can often be visible to the naked eye, not all disabilities are so easily recognized. Chronic pain or a mental health issue can also qualify as a disability.

How does it work?

- Choose the amount you want and add optional benefits to customize your coverage.

- Pay your monthly premium.

- File a claim if you become disabled.

- Receive your monthly income payments when the waiting period ends. The waiting period is the number of days from the date you’re disabled until the benefit start date.

- Your income payments stop when your benefit period ends or you return to work.

Why do you need Disability insurance?

![]()

It’s more common than you think

Up to 40% of Canadians become disabled for 90 days or longer before age 65.

![]()

Replaces most of your paycheque

Potentially you can receive up to 80-90% of your take-home pay.

![]()

Protect your retirement savings

Disability insurance can help you meet your financial obligations so you may be able to avoid dipping into your retirement savings.

Protect your most valuable asset

Your ability to earn an income over a 30- or 40-year career is your most valuable asset. Consider your current income, indexed to inflation, from your current age to age 65. This amount of potentially lost income can easily be measured in the millions of dollars.

How much does it cost?

Premiums often range from 1-9% of your salary, but each case is different. Here are some factors that can affect cost:

- Coverage amount – The more you’d like to receive, the more it will cost.

- Benefit period – It’ll cost more the longer you want to receive payments.

- Waiting period – Your premiums will be less expensive if you’re willing to wait longer to receive payments.

- Age – Disability insurance may be less expensive when you’re young.

- Health – Your costs will be lower the healthier you are.

- Occupation – If you have a dangerous job, your premiums can be higher.

How much income can you get?

For most people, the maximum limit that you can insure your income for is around 66% of your average pre-tax income over the past two years. This can depend on other circumstances such as your age and occupation.

However, since the premiums paid for a personal Disability insurance plan are paid with after-tax income, the income benefit received is tax free, so 66% of your pre-tax income can be very close to all of your normal take-home pay.

What does the government give you?

You can get disability coverage through the Canada Pension Plan (CPP) and Quebec Pension Plan (QPP), but they provide limited benefits.

Strict definition

You must “have a severe and prolonged mental or physical disability” to qualify for CPP disability benefits. You may be able to get personally owned disability coverage under a much more relaxed definition. Personally owned disability coverage is easier to activate and far easier to keep activated.

Lower monthly benefit

The CPP’s average monthly benefit is $966.43, and the maximum in 2019 is $1,362.30. Is this enough coverage in the event of a prolonged disability for you and your family?

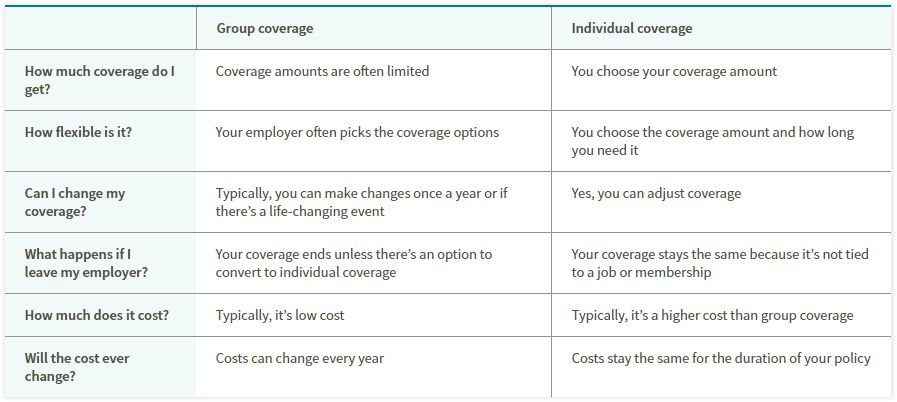

Do you need disability insurance if you have it through your employer?

Group insurance is a great start, but it usually only provides basic coverage. A personal disability policy complements group insurance – together, they can help protect you, your family, and your lifestyle should the worst happen.

Do you need Critical illness or Disability insurance?

Depending on your situation you may need only Critical illness or Disability insurance but there are many times when you need both to fully protect yourself. Critical illness and Disability insurance work differently – but together – to help reduce the financial impact of disability or serious illness.

If you found the information on this page useful, please give it a quick “like” or share it with someone else who may find it helpful:

Contact me for more information and to help determine what makes the most sense in your situation.